What is car finance GAP insurance?

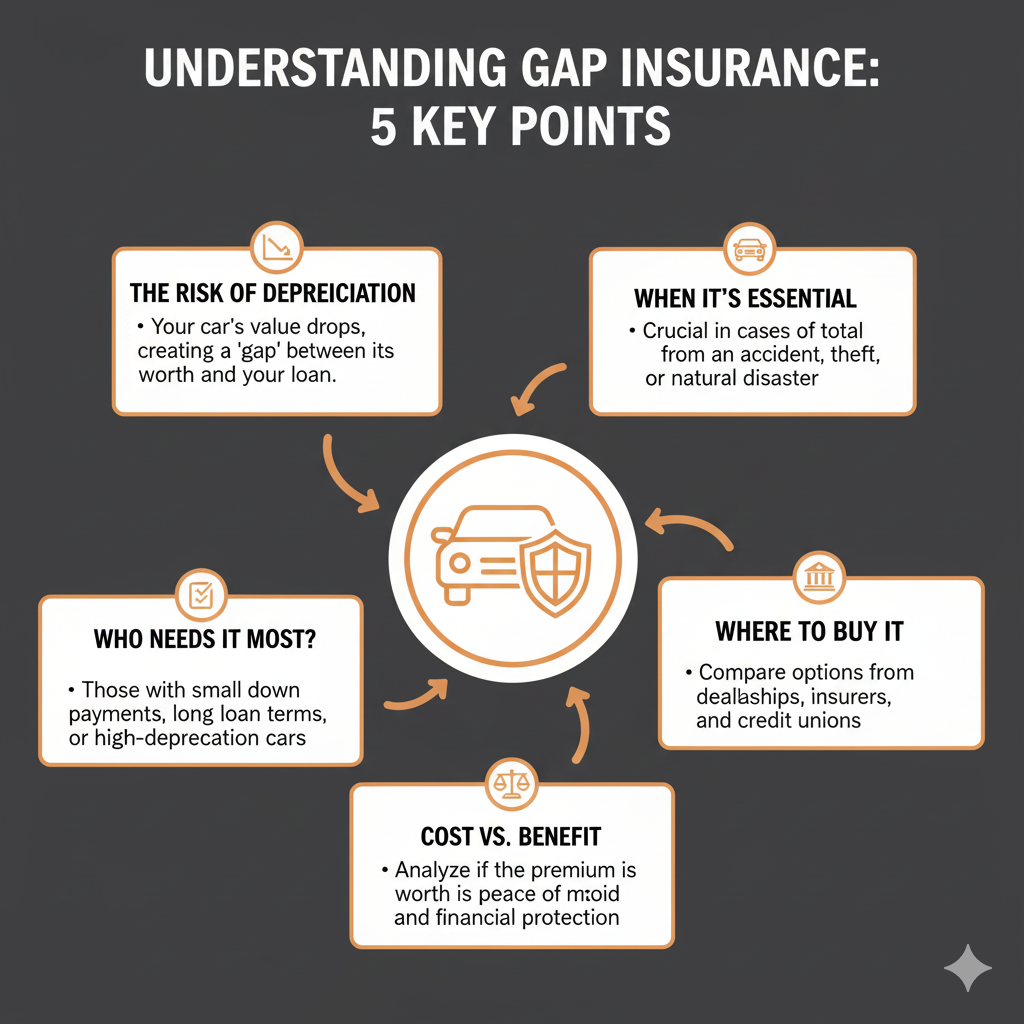

It’s fun to buy a new car, but the cost can be sobering. As soon as you leave the dealership, your car’s value goes down a lot. This drop in value could leave you with a gap between what you owe on your car loan and what your car is actually worth. GAP insurance fills this gap and protects you from losing a lot of money that could be very bad for you.

When you’re paying for a car, it’s very important to understand GAP insurance. Standard auto insurance pays for the current market value of your car, but this amount may not be enough to cover the amount you still owe on your loan. If you don’t have enough money, you might have to pay for a car you no longer own while also needing money for a new one.

Guaranteed Asset Protection (GAP) insurance is a way to protect your money. It pays for the difference between the cash value of your car at the time of loss and the amount you still owe on your auto loan or lease. This protection is especially useful in the first few years of owning a car, when it loses value the fastest.

A lot of people who buy cars don’t know about this coverage option until it’s too late. If you learn more about how GAP insurance works, you’ll be able to decide if it’s the right kind of protection for your finances and how much risk you’re willing to take.

The Need for GAP Insurance Starts with Understanding Car Finance

There are different types of car loans, and each one has a different level of risk for negative equity. With a traditional auto loan, you can buy a car by borrowing money and paying it back over time, usually between three and seven years. You own the car during this time, but you use it as collateral for the loan.

Lease agreements work in a different way. You’re basically renting the car for a set amount of time, which is usually between two and four years. When the lease ends, you can give the car back, buy it for the residual value, or sometimes extend the lease. GAP insurance can help both ways of getting money.

The depreciation timeline applies to all vehicles, but it changes depending on the make, model, and market conditions. Luxury cars tend to lose value more quickly at first, but some brands keep their value better over time. Electric vehicles are different because their value can go down in ways that are hard to predict because technology changes quickly and market preferences change.

The amount of your down payment has a direct effect on how much GAP insurance you need. From day one, larger down payments lower the loan-to-value ratio, which may mean that you don’t need GAP coverage as soon. On the other hand, if you put down little or no money, you are more likely to end up with negative equity, which makes GAP insurance more useful.

The Risk of Negative Equity: When You Owe More Than Your Car Is Worth

When your loan balance is higher than the current market value of your car, you have negative equity. This is a common problem for new car owners because cars lose value quickly. This is also referred to as being underwater or upside down on your loan.

There are a number of things that speed up the growth of negative equity. Longer loan terms mean lower monthly payments, but they also mean you’re paying off the principal more slowly. High interest rates make this problem worse by making it so that more of your early payments go toward interest instead of paying down the principal. If you roll over negative equity from an old car loan into a new one, there is an immediate and big gap.

Market conditions have an unpredictable effect on depreciation rates. Changes in gas prices, economic downturns, or changes in what people want can have a big effect on some types of cars. For example, when gas prices go up, big SUVs and trucks may lose value faster than small cars that get good gas mileage.

Negative equity has effects that can be seen in real life. Think about getting a $30,000 car with a $2,000 down payment and paying off the rest over six years. You might owe $25,500 after a year, but the car is only worth $22,000. If the car is totaled or stolen, this $3,500 difference is what you could lose.

Important Situations Where GAP Insurance Is Necessary

In cases of total loss, GAP insurance shows its true worth. If your car is declared a total loss because of an accident, theft, or natural disaster, standard comprehensive and collision coverage only pays the car’s actual cash value. You are still responsible for the difference if this amount is less than your loan balance.

Think about Sarah, who bought an SUV for $35,000 with a small down payment. Her car was destroyed in a flood eighteen months later. The insurance company gave her $26,000 based on the car’s lower value, but she still owed $31,000 on her loan. Sarah would have had to pay $5,000 for a car she could no longer drive if she didn’t have GAP insurance.

Theft scenarios pose analogous challenges. Car thieves these days often go after newer, popular models that may be too damaged to fix for a reasonable price. Even if the items are found, if they are badly damaged, they may be declared a total loss, which would trigger the same GAP insurance benefits as if they were stolen.

Disasters caused by the weather lead to a lot of GAP insurance claims. Hurricanes, floods, hailstorms, and wildfires can all destroy thousands of cars at the same time. GAP coverage is especially useful in areas that are prone to disasters because these events often happen to newer cars that owners are still paying for.

Another example of GAP insurance is ending a lease early. If you need to end your lease early because you have to move for work, are having trouble paying your bills, or for any other reason, early termination fees can be very expensive. Some GAP policies cover these costs.

Choosing the Right Type of GAP Insurance

Loan GAP insurance pays the difference between the actual cash value of your car and the amount you still owe on it. This simple coverage works for regular car loans and covers the most common case of negative equity. The policy pays the difference directly to your lender, so you don’t have to pay the rest of the balance.

Lease GAP insurance works in a similar way, but it covers situations that are specific to leases. It might also cover the difference between the actual cash value and the remaining lease payments, as well as early termination fees, extra wear and tear charges, and other lease-related obligations. This all-encompassing method protects against the different financial penalties that can happen when a lease ends.

New car replacement GAP insurance is more than just basic gap coverage. This coverage pays for a brand-new model of the same make and model to replace your totaled vehicle, not just the difference between the actual cash value and the loan balance. This premium option costs more, but it gives owners who want full replacement coverage better protection.

Return-to-invoice GAP insurance, which is popular in some places, pays the difference between the insurance settlement and the vehicle’s original invoice price. This type of coverage gives you a clear idea of how much protection you’ll have, but it might not cover negative equity that comes from long loan terms or high interest rates.

Some GAP policies offer extra benefits, such as coverage for rental cars, help with deductibles, or coverage for accessories that you buy after the fact. These extra features raise your premiums, but they give you better protection that fits your needs and wants.

Important Things to Think About Before Buying GAP Insurance

The value of your GAP insurance is greatly affected by the loan-to-value ratio at the time of purchase. To figure this out, divide the amount of your loan by the value of the car. If your ratios are above 90%, it means that your GAP insurance benefits are higher. If your ratios are below 80%, it means that you might not need coverage as much, especially if you’re buying a car that will sell well.

The rate at which vehicles lose value is very different in different segments. Use automotive guides and market analysis reports to find out what the expected depreciation curve is for your specific make and model. Over time, cars that lose value more slowly naturally lower the value of GAP insurance.

The terms of the loan have a direct effect on how much GAP coverage you need. Longer loan terms slow down the process of paying off the principal, which means you could owe more than the car is worth for a longer time. GAP coverage is almost always a good idea for six- and seven-year loans, but it might not be necessary for three-year loans.

GAP insurance depends on how you drive and how you live. Drivers with a lot of miles on their cars speed up depreciation, which could make negative equity periods last longer. GAP coverage is more useful for city drivers because they are more likely to have their cars stolen or get into accidents. On the other hand, cars that are kept in garages in low-crime areas by careful drivers may not need as much coverage.

People who are financially stable make decisions about GAP insurance. GAP insurance gives you peace of mind if losing several thousand dollars would be a big financial problem for you. But if you have a lot of money saved up for emergencies and can easily make the gap payments, you might want to self-insure against this risk.

Knowing how much GAP insurance costs: protection vs. investment

The cost of GAP insurance depends on a number of things, such as the type of vehicle, the amount of the loan, the level of coverage, and the provider. A one-time payment of $500 to $800 is usually required for dealership GAP insurance. For your convenience, this fee is often included in your financing. This method spreads the cost over the life of the loan, but the GAP premium does come with interest charges.

When added to your current auto policy, insurance company GAP coverage usually costs less, between $20 and $40 a month on average. You can cancel coverage once your negative equity is gone with this pay-as-you-go plan. This could save you money over the life of the loan.

Credit union GAP insurance is often the best deal for members. Full coverage costs between $200 and $400. These member-focused organizations usually have competitive rates and good policy terms, which makes them a good choice for eligible buyers.

Standalone GAP insurance companies are another option, especially for people who have special needs or can’t get coverage through regular channels. These specialized companies may offer more flexible terms or coverage for modified vehicles, but prices can be very different.

The break-even analysis helps you figure out how much GAP insurance is worth. Figure out how much gap exposure you might have during the life of your loan and compare that to the total cost of GAP insurance. The coverage is a good deal if the maximum gap exposure is much higher than the GAP premiums. If gap exposure stays low, you might want to use other ways to manage risk.

Finding the right amount of GAP insurance: weighing cost and protection

GAP insurance is most useful when you have the most negative equity, which is usually the first two to three years after you buy a car. During this time, fast depreciation and slow principal paydown together create the biggest gap exposure. Find out how long it will take you to break even on the loan balance and the value of the car.

Think about how much risk you’re willing to take with your money and how much money you have set aside for emergencies. GAP insurance basically moves the financial risk from you to the insurance company. If you might have to borrow money or put a strain on your finances because of a possible gap, GAP coverage is a good idea. On the other hand, if you have enough money set aside for emergencies, you might want to keep this risk.

Making bigger down payments, choosing shorter loan terms, or picking cars with better resale values are all other ways to lower your risk. These methods naturally lower the risk of gaps, but they may not get rid of them completely. The best way to protect yourself is to use these strategies along with GAP insurance.

The value of GAP insurance changes depending on where you live because of different disaster risks, crime rates, and market conditions. GAP insurance benefits are higher in places that are likely to have natural disasters, high rates of car theft, or unstable used car markets. In areas that are stable and low-risk, it might make sense to have less coverage.

Don’t forget about the peace of mind factor. Unexpected big bills can cause financial stress that can hurt your health, your relationships, and your job performance. GAP insurance takes away the stress of having to pay for a car you can’t drive, so you can focus on getting better and getting a new car.

How to Get GAP Insurance: Looking at Your Choices

GAP insurance from a dealership is easy to get and covers you right away, but it usually costs more than other options. Dealers may say that GAP insurance is necessary or urgent, but you usually have time to look at other options. Before you agree to dealer-provided coverage, make sure you know the specifics of the policy, what it doesn’t cover, and how to cancel it.

GAP coverage is often offered by auto insurance companies as an extra to comprehensive and collision coverage. This method combines all vehicle coverage into one policy, making it easier to file claims and make payments. Talk to your current insurance company about GAP options, as you may be able to get a discount as an existing customer.

Credit unions and banks often offer loan customers GAP insurance rates that are hard to beat. These banks and credit unions know everything about your finances and might give you discounts if you use more than one service. Credit unions and community banks put more emphasis on providing value to their members than on making the most money.

Online GAP insurance companies have become good options because they offer good rates and easy ways to apply. These businesses are experts in GAP coverage and may offer more flexible terms or coverage for special situations. Before buying online coverage, look into the stability and claims-paying ability of the provider.

When you buy GAP insurance, timing is important. Most providers require you to buy coverage within 30 to 90 days of getting your car or taking out a loan. Some insurance companies will cover things you bought recently, but the options get fewer as time goes on. If you think GAP insurance is right for you, don’t wait.

Choosing the Best Path for Your Financial Future

GAP insurance is one part of full financial protection for car owners. Your financial situation, how much risk you’re willing to take, and the type of car you have all play a role in whether or not you should buy coverage. Most financial experts say that people who make small down payments, have long loan terms, or buy cars that lose value quickly should get GAP insurance.

Use online calculators or talk to financial experts to figure out how much of a gap you might be exposed to. Look at the costs of GAP insurance from different companies, taking into account both the initial premiums and the ongoing costs. When making your final choice, think about how much money you have in your emergency fund and how stable your finances are overall.

Keep in mind that your needs for GAP insurance may change over time. As you pay off your loan and your car loses value more slowly, your gap exposure naturally goes down. GAP insurance is a flexible way to protect yourself because many policies let you cancel and get your money back for coverage you didn’t use.

GAP insurance is something you should think about as part of your overall plan for managing financial risk. GAP insurance can help protect you from unexpected financial problems when you have enough emergency funds, the right auto insurance, and make smart decisions about how to pay for things.

New products, technologies, and market conditions are always changing the way people get car loans. Keep up with changes that could affect your GAP insurance needs, like incentives for electric vehicles, new coverage options from providers, or changing patterns of depreciation.

Common Questions About GAP Insurance

Does GAP insurance pay for finance fees and interest?

Most GAP insurance policies cover the simple interest that is part of your loan payoff amount, but they don’t cover late fees, extended warranty costs, or credit life insurance premiums. Look at the wording of your policy to see exactly what costs are included in gap calculations.

If I have full coverage auto insurance, do I still need GAP insurance?

Full coverage auto insurance includes both comprehensive and collision coverage, but it only pays the actual cash value of your car at the time of loss. The amount you owe may be less than your loan balance, which is a gap that regular insurance doesn’t cover. GAP insurance is meant to cover this difference.

How can I tell if my car loan has GAP insurance?

Look at your loan papers, insurance policy declarations, or call your lender directly. Your financing paperwork or insurance policy should clearly show that you have GAP coverage. Both your lender and your insurance agent can check to see if you have coverage if you’re not sure.

When does GAP insurance not cover claims?

GAP insurance usually doesn’t cover missed payments, balances from previous loans that carry over, extended warranties, or coverage for mechanical breakdowns. If you commit fraud, race, or use your car for business, your coverage may also be void. Each policy has certain exclusions that spell out the limits of coverage.

Can GAP insurance help you purchase a new vehicle?

GAP insurance takes away your financial responsibility for a totaled car, but it doesn’t give you money to buy a new car. However, GAP coverage improves your financial situation for getting new loans by paying off your old loan balance and not carrying over negative equity.