Loan Risks Every Small Business Owner Should Know

For any small business, getting a loan can feel like a big step forward. It can help businesses grow, pay for expansion, and give them the money they need to get through tough times. But borrowing money is a big financial decision that comes with its own set of problems. Someone who starts and runs a business knows that every choice matters, and getting financing is no different. It’s not just a good idea to know the risks of borrowing money; it’s necessary for long-term survival and success.

A lot of business owners think about the benefits of starting their own business, but they also need to be very aware of the risks, especially when they need money from outside sources. If a business owner doesn’t fully understand the risks that come with taking out a loan, they could unknowingly put their company’s financial health, personal assets, and future viability at risk. This guide will show you all the different loan risks you might face and explain what they mean for your business in detail.

We will look at the different kinds of loans that small businesses can get, talk about the most common loan risks, and give you practical tips on how to deal with them. By the end of this post, you’ll know more about how to make smart borrowing choices, keep your money safe, and confidently guide your business towards a stable and successful future.

What kinds of loans can small businesses get?

It’s important to know how financing works before you start talking about the risks. The kind of loan you take out will affect the risks you take on. Here are some of the most common financing options for small businesses:

- Loans from the SBA: Partner lenders offer these loans with the help of the U.S. Small Business Administration. They usually have good terms, like lower interest rates and longer times to pay back the loan. But the application process can be hard, and they usually need a lot of paperwork.

- Term loans are regular loans where you get a set amount of money up front and pay it back with interest over a set amount of time. Term loans are great for making big purchases, like buying equipment or real estate, all at once. You can get them with or without collateral.

- Business Lines of Credit: A line of credit is like a credit card in that it gives you access to a certain amount of money that you can use whenever you need it.Interest is only charged on the money you use. This choice is flexible and works well for dealing with changes in cash flow or unplanned costs.

- Equipment financing is a type of loan that is specifically for buying business equipment. The equipment itself is used as collateral. This might make it easier to get than other kinds of loans.

- Invoice Financing: If your business has unpaid bills, you can sell them to a financing company for less than what they’re worth and get cash right away. This helps fill the gap between sending invoices and getting paid.

- Merchant Cash Advances (MCAs): An MCA gives you a one-time payment in exchange for a percentage of your future credit and debit card sales. They are easier to get and give you quick access to cash, but they often have very high effective interest rates.

Common Loan Risks and Their Consequences

Getting a loan is a big deal, but it also means you have to take on new responsibilities. If you know what risks come with borrowing money, you can get ready for them and deal with them better. Here are the key loan risks every small business owner should be aware of.

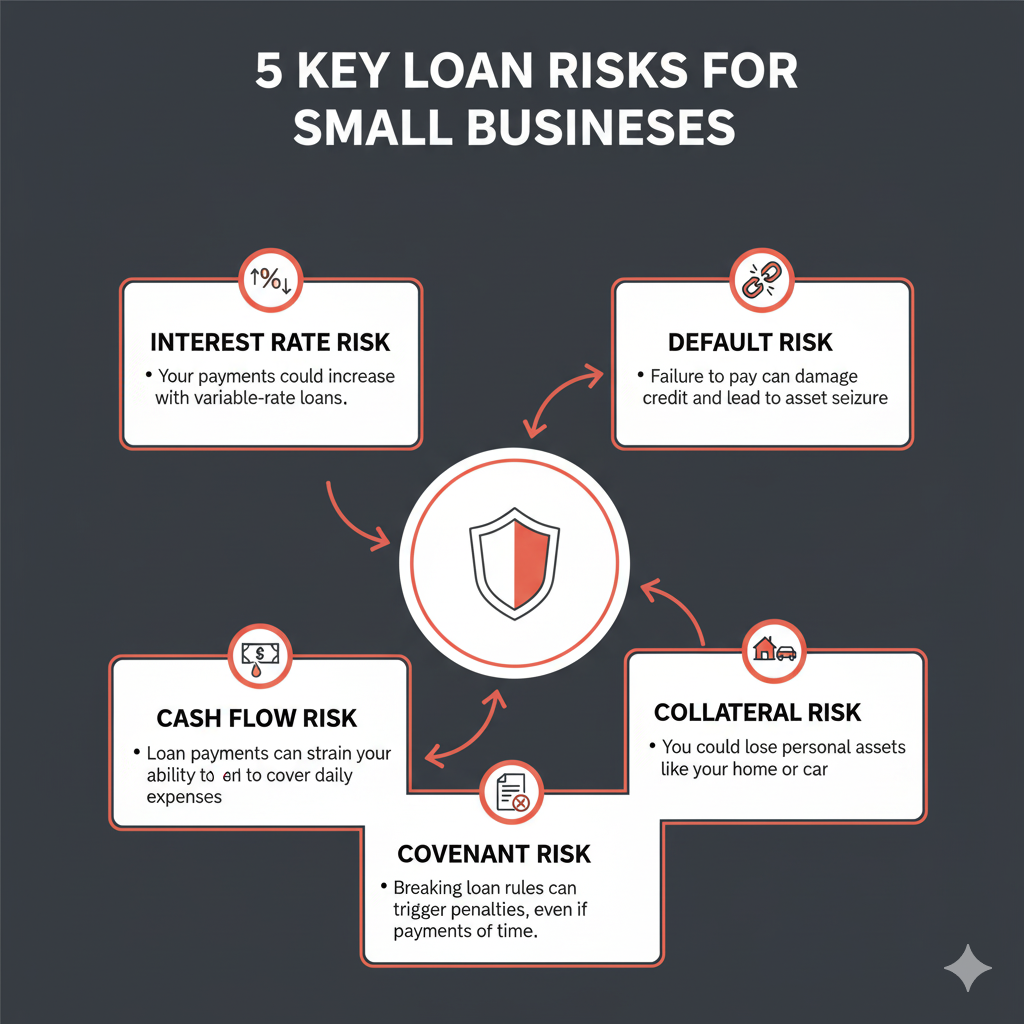

Risk of Interest Rates

The cost of borrowing money is set by interest rates. There are two main types of this risk: fixed rates and variable rates.

- With fixed-rate loans, the interest rate stays the same for the whole loan term, so your payments will stay the same. This makes it easier to budget because it gives you stability and predictability.

- Variable-rate loans have interest rates that can change based on a benchmark index, such as the prime rate. The initial rate might be lower than that of a fixed-rate loan, but it could go up over time. If interest rates suddenly go up, your monthly payments could go up a lot, which would make it hard for you to pay your bills. When deciding if a small business owner can safely pay for a new project, this is a very important financial risk to think about.

Risk of Default

Default risk is the possibility that your business will be unable to make its loan payments. Not paying back a loan has serious consequences:

- Damage to Credit Score: Your business and personal credit scores can both drop a lot, making it hard to get loans in the future.

- Seizure of Collateral: If you put up collateral for the loan, the lender can take those things back to make up for their losses.

- Legal Action: If you don’t pay your debt, lenders can take you to court, which could mean that your wages are taken or that liens are put on your property.

- Business Failure: In the end, a business may have to close because it can’t afford to pay back a loan. A business owner could lose all of their money.

Risk of Cash Flow

This is the risk that your business won’t make enough money to pay for its costs, such as loan payments. A business that makes money can still go out of business if it runs out of money. Taking out a loan raises your monthly fixed costs, which makes it easier for your business to run out of cash. If you don’t have enough cash on hand to pay your loans, a sudden drop in sales, a delay in customer payments, or a sudden rise in costs can quickly lead to a crisis.

Risk of Collateral

A lot of loans, especially for new businesses or those with bad credit, need collateral. You promise the lender that you will give them collateral, which is an asset like real estate, equipment, or inventory, as security for the loan. The lender can take it if you don’t pay.

The main risk is easy to see: what could small business owners lose if their business goes under? A lot of the time, the answer includes personal property. If the business can’t pay back the loan, you are personally responsible for the debt if you signed a personal guarantee. This puts your car, home, and personal savings at risk.

Covenant Risk

Loan covenants are rules or conditions that lenders put in a loan agreement. The purpose of these rules is to protect the lender’s investment by making sure the borrower stays financially stable. Some common covenants are:

- Keeping a certain ratio of debt to equity.

- Keeping a certain amount of working capital.

- Giving out regular financial reports.

- Not letting the business take on more debt without permission.

Breaking a covenant, even if you are still making your payments on time, can cause a technical default. This could let the lender ask for the full loan amount right away or raise your interest rate.

Ways to Reduce the Risks of Loans

The first step is to know the risks. The next is implementing strategies to manage them. Taking a proactive approach to managing risk can mean the difference between a loan that helps your business grow and one that sinks it.

1. Make a detailed financial plan

Make detailed financial projections before you even apply for a loan. Before starting any business or big project, you should ask yourself these three questions: These often have to do with the need in the market, how profitable it will be, and whether it can be done. Your financial forecast should tell you how much money you really need.

- The money will be used for what purpose?

- How will the investment make money?

- Can you easily pay the new loan payments with the cash flow you expect?

A good business plan with realistic estimates will not only help you get approved, but it will also help you figure out how to pay off the debt.

2. Keep a steady cash flow

For a reason, cash is king. To lower the risk of cash flow problems, pay attention to:

- Keeping a close eye on your cash flow: Keep track of your income and expenses with accounting software.

- Setting up a cash reserve: In case of an emergency, you should have saved up enough money to cover at least three to six months’ worth of expenses.

- Managing accounts receivable: Send invoices to customers right away and follow up on late payments.

- Keeping costs down: Look over your budget often to see where you can save money.

3. Get the best terms for your loan

Don’t just take the first loan offer you get. Compare interest rates, fees, and repayment terms by shopping around with different lenders. When you are negotiating, be very careful about:

- Rate of Interest: If you can, choose a fixed rate so you know how much you’ll have to pay each month.

- Time to pay back: Longer repayment periods mean lower monthly payments, which can help with cash flow, but you’ll end up paying more in interest over time. Find a balance that is good for your business.

- Covenants: Read the small print. Make sure you know what all the covenants mean and that they are doable for your business.

- Fees for Paying Early: See if there is a fee for paying off the loan early.

4. Know and follow the terms of your loan

You need to keep an eye on your compliance with all loan covenants to avoid a technical default. To make sure you’re meeting the lender’s requirements, work closely with your accountant to keep track of important financial ratios. If you think there might be a breach, get in touch with your lender right away. They might be willing to let you change the loan agreement or give you a temporary waiver.

5. Get money from different places

It can be dangerous to depend on just one source of money. Look into a variety of ways to get money to make your capital structure stronger. You could, for instance, use a term loan to buy a lot of equipment and keep a business line of credit for your daily cash flow needs. This diversification can help protect you if one source of funding goes away. This is a key part of how to deal with risk in business.

Confidently Making Your Borrowing Choices

One of the most important choices a small business owner can make is to take on debt. There are many important moments in the life of someone who starts and runs a business and risks both time and money. Loans can help your business grow in amazing ways, but they also come with big risks that could put everything you’ve worked for at risk. These problems, like changing interest rates, cash flow problems, and the risk of losing collateral, need to be thought about carefully and managed ahead of time.

You can feel good about getting a loan if you know about the different types of loans, the risks that come with borrowing, and how to protect yourself from those risks. The best ways to avoid problems are to plan ahead, keep a close eye on your cash flow, and really understand your loan agreement.

Keep in mind that getting a loan is more than just a transaction; it’s a business relationship with your lender. If you build a strong, open relationship, you’ll have the freedom and support you need to deal with any problems that come up.