What will the next RBNZ decision mean for your mortgage?

The phrase “OCR announcement” probably catches your eye if you own a home or want to buy one in New Zealand. The Reserve Bank of New Zealand (RBNZ) sets the Official Cash Rate, which has a big impact on how much you pay for your mortgage. Homeowners and financial experts alike keep a close eye on every RBNZ interest rate decision because the economy is always changing.

This guide will tell you what the RBNZ does, what factors will affect its next decision, and how that could affect your mortgage. You will be able to make better financial decisions and feel more confident in New Zealand’s real estate market if you understand these factors.

The state of New Zealand’s economy right now

Before we can guess what the RBNZ will do next, we need to know what the economy is like right now. There are a few important things that are currently affecting its thoughts:

- Inflation: The RBNZ’s main goal is to keep prices stable, which means keeping inflation between 1% and 3%. Inflation has been a big worry lately, which is why the RBNZ has had to be tough. Inflation is still a big deal, even though it has started to go down. If prices keep going up, the RBNZ may keep interest rates high.

- Economic Growth: The RBNZ needs to find a balance between fighting inflation and supporting economic activity. When interest rates are high, it costs businesses and consumers more to borrow money, which can slow down the economy. The bank will keep a close eye on GDP numbers, unemployment rates, and business confidence to make sure that its policies aren’t making things worse for no reason.

- Things that happen around the world: The economy of New Zealand doesn’t work in a vacuum. Things that happen in other countries, like problems with the supply chain, tensions between countries, and the economic policies of major trading partners, all have an effect. When the RBNZ decides what to do with interest rates, it thinks about these global trends.

The RBNZ has a hard time putting these pieces together. Its next OCR announcement will show what it thinks is the biggest threat to New Zealand’s economic stability.

Possible Outcomes for the Next OCR Announcement

The RBNZ can either keep the interest rate the same, raise it, or lower it. Each option would send a different message to the market and have different effects on people with mortgages.

For example, Scenario 1: The RBNZ Keeps the OCR

A decision to hold the OCR would suggest the RBNZ believes its current monetary policy is appropriate for the economic conditions. If inflation is going down as expected but hasn’t yet hit the target range, this is the most likely thing to happen.

- Many economists think that the RBNZ will keep the OCR steady for most of 2024, waiting for clear signs that inflation is under control before thinking about cutting it.

- Immediate Effect: If rates stay the same, floating mortgage rates probably won’t change much right away. But banks may change their fixed-rate offers based on how much it costs them to borrow money and what they think will happen in the future.

The RBNZ raises the OCR in Scenario 2.

If the OCR goes up, it would mean that the RBNZ is still very worried about inflation. This would be a hawkish move to cool the economy even more and lower prices.

- Prediction: At this point, a rate hike seems less likely unless new data shows that inflation is rising faster than expected.

- Immediate Effect: Banks would almost certainly pass on the increase to customers with floating or variable-rate mortgages. The price of new fixed-rate mortgages would probably go up too.

Scenario 3: The OCR Goes Down for the RBNZ

If the RBNZ cuts the OCR, it would mean that they are sure that inflation is under control and are now focusing on boosting economic growth. This is what most people who have mortgages want to happen.

- Prediction: Most analysts do not expect an OCR cut until late 2024 or even 2025. The RBNZ has said it wants to be sure that inflation is under control before it makes policy changes.

- Immediate Effect: A cut would lower the rates on floating mortgages. Banks might also lower fixed rates because they think rates will go down even more in the future.

What will this mean for your mortgage?

The type of mortgage you have will greatly affect how the RBNZ’s decision affects you.

In the event that you have a floating mortgage

Changes in the OCR have a direct effect on your interest rate. If the RBNZ raises the rate, your payments will go up quickly. You’ll notice the difference right away if it cuts the rate. If you hold, your rate will probably stay the same. This structure is flexible, but it also has some risks.

If You Have a Mortgage with a Fixed Rate

If your mortgage is fixed right now, your payments won’t change until the fixed term ends. When you need to re-fix, the RBNZ’s decision is the most important. The new fixed rates will be higher if the OCR is high or is expected to go up. You might be able to lock in a much lower rate if the OCR is going down.

If You’re Close to Negative Equity

When the value of your property drops below the amount you still owe on your mortgage, you have negative equity. While the RBNZ mortgage rules and bank lending criteria are designed to prevent this, a sharp drop in house prices combined with high interest rates can put recent buyers at risk. An OCR hike would increase this pressure by raising repayments for those on floating rates.

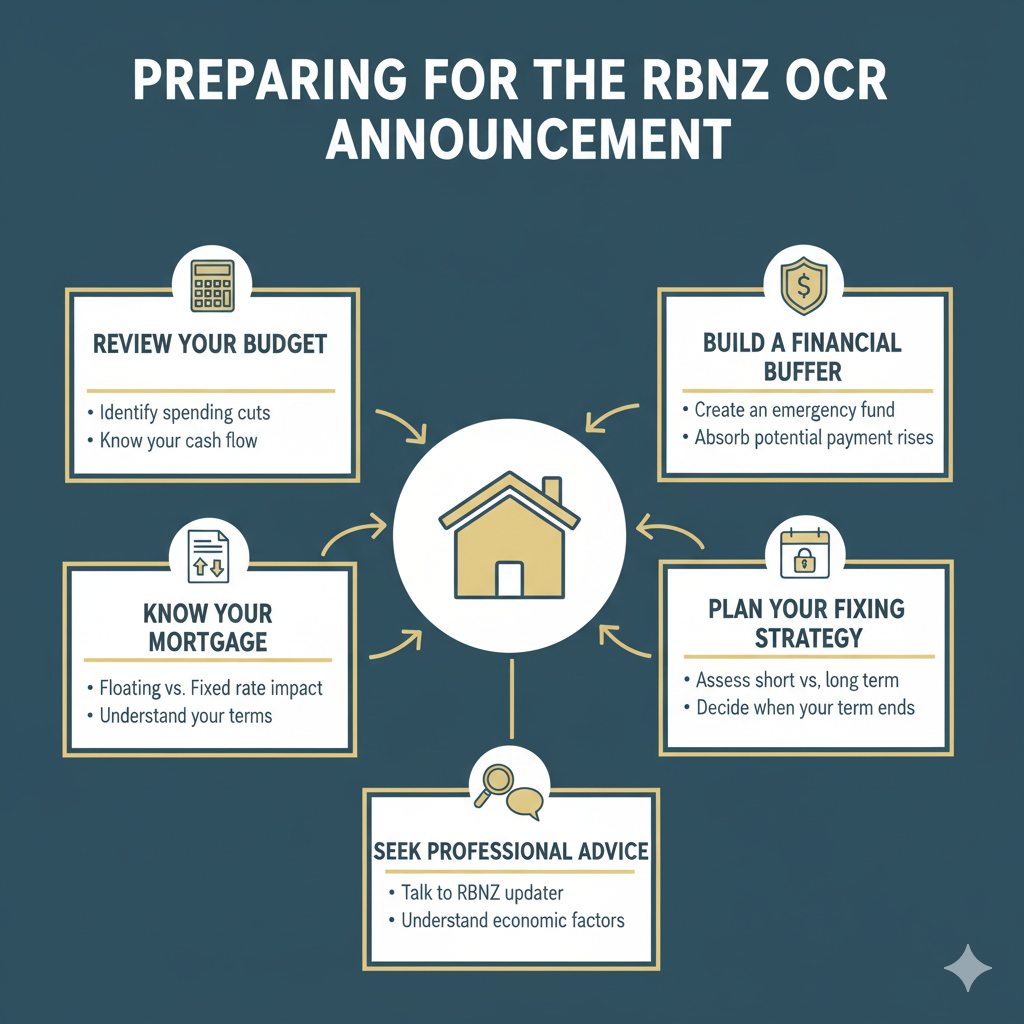

How to Get Your Money Ready

You can protect your financial health no matter what the RBNZ decides.

- Look over your budget: Understand exactly where your money is going. If rates go up, you’ll need to know where you can cut back on your spending.

- Build a Buffer: Make an effort to set aside some money for emergencies. If your mortgage payments go up, having some extra money can help you relax.

- Think about how you plan to fix things: If your fixed term is ending, think carefully about your options. If you think rates will go down soon, it might be better to fix for a shorter time, like a year. A longer-term fix provides more certainty but could mean you miss out if rates drop.

- Get in touch with an Advisor: Don’t decide these things by yourself. A financial advisor can help you understand the market, assess your risk tolerance, and choose the best strategy for your situation.

Finding your way through your financial future

The RBNZ’s decision about interest rates is very important for all homeowners in New Zealand. While predicting the exact outcome is difficult, understanding the potential scenarios and their impact on your mortgage is the first step toward sound financial planning. You can confidently deal with the changing interest rate environment by staying informed, going over your budget, and getting professional advice.

The Business Kiwi team is here to help if you have questions about your mortgage or want to talk about a plan that fits your financial goals. Call us today to set up a meeting and get expert advice on how to buy a home.